African startups are on track to raise more funding in 2025 than in 2024. Startups on the continent have raised $2.8 billion so far this year (January-August), equaling the total amount raised in 2024, according to Briter Intelligence data.

“I think it's a recovery. So it's just a typical boom-bust cycle,” said Fisayo Durojaiye, an African-focused Investment professional.

As investors appear to be regaining confidence in the continent’s tech ecosystem, fintech, cleantech, and mobility have attracted the largest share of deals so far, with fintech securing over $1 billion and cleantech close behind at $950 million.

Unlike in previous years, where equity overwhelmingly led funding structures, 2025 has seen debt financing exceed the $1 billion milestone for the first time. This signals a maturing ecosystem with increasingly asset-heavy, scaled businesses leveraging non-dilutive instruments for growth.

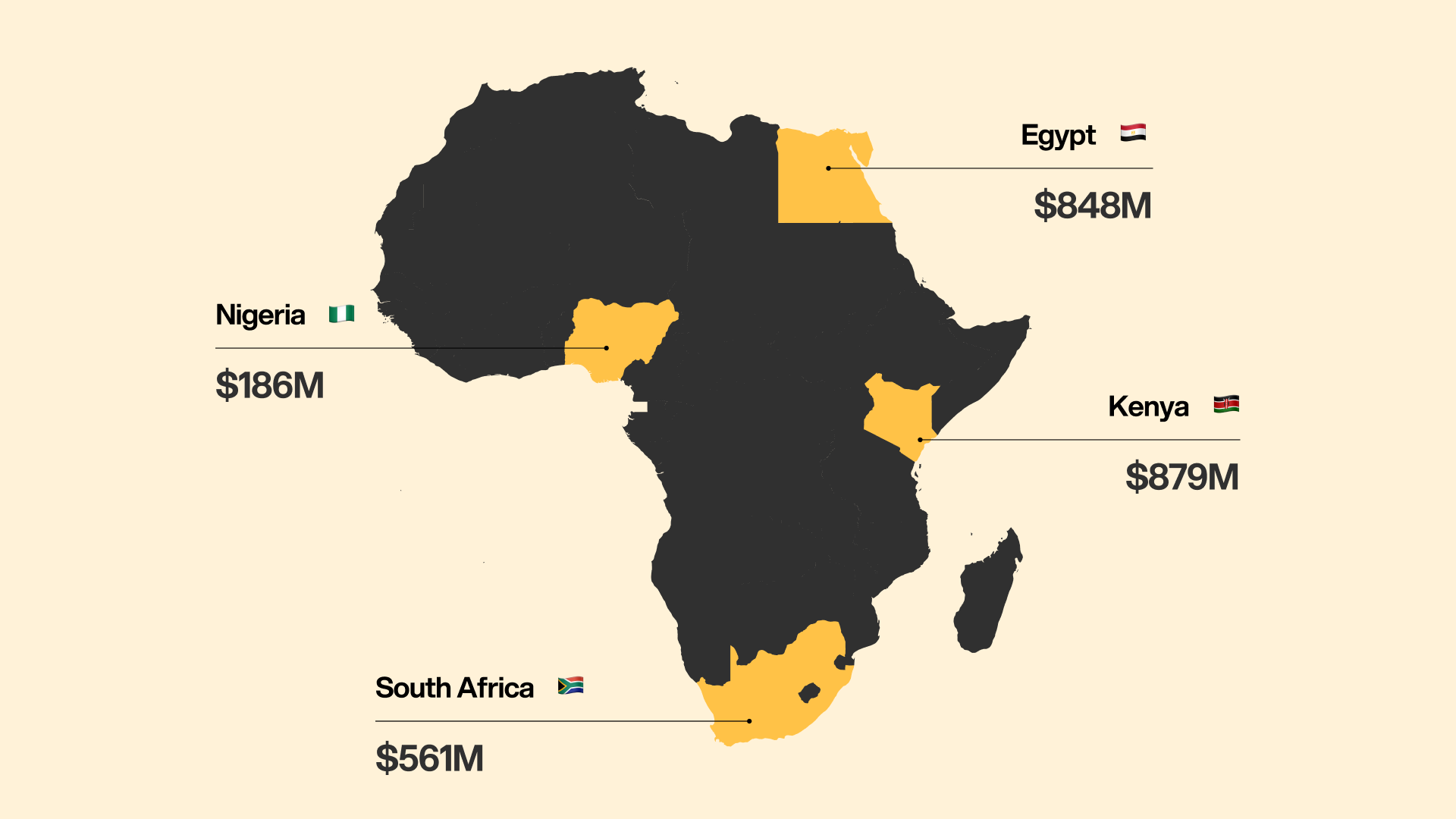

Geographically, East and Southern Africa emerged as the top-funded regions, attracting $865 million and $845 million, respectively, with West ($450+ million) and North Africa ($420+ million) falling behind in dollar terms but maintaining high deal counts. Nigeria’s early-year momentum tapered, while South Africa and Kenya hosted most of the mega-rounds and significant buyouts.

Major deals that shaped the year include: Kenya’s solar energy company d.light $300 million debt; Sun King ’s $236 million debt; South Africa’s Zepz $165 million debt; Solar Africa ’s $98 million equity; and NedBank’s $93 million acquisition of iKhokha .

There were over 40 acquisitions and 6 company shutdowns recorded so far this year, with notable M&A activity on the continent including Meta’s acquisition of Egypt’s PlayAI, Lesaka’s $60M+ purchase of South Africa’s Bank Zero and NedBank’s $93 million acquisition of iKhokha .

Let’s take a closer look at the key trends driving Africa’s investment momentum across sectors and regions.

1. A Shift towards larger deals.

Despite a continued decline in the overall number of deals since the 2022 funding bubble, the deals that are closing in 2025 are notably larger, pushing the median check size higher. As a result, the total disclosed funding for the first eight months of the year has already doubled compared to the same period in 2024.

The median deal size for 2025 so far aligns with that of 2022, suggesting a reduction in early-stage or sub-$1 million rounds and a shift towards supporting established ventures. However, sub-$250k investment rounds sharply declined: only 21 so far this year versus 90 in 2022.

While fintech continues to lead the way with over 115 deals, other sectors like education (65+), agriculture (50+), health (45+), and cleantech (35+) are also drawing significant investor interest, underscoring a broadening of capital flows beyond traditional fintech dominance.

2. Fintech remains dominant, but cleantech is on the rise.

Fintech continues to attract the largest share of both investments and deal volume. However, cleantech has seen the fastest year-on-year growth, driven largely by debt financing. This year, cleantech deals accounted for nearly half of all funding in February and dominated July, securing almost 80% of capital through debt deals.

So far, fintech has raised over $1 billion, with cleantech close behind at $950+ million. Nearly half of the cleantech funding so far went to two companies (Sun King and d.light). Healthtech has attracted $150 million, while mobility and property tech have raised $100+ million and $75+ million, respectively.

3. Debt Financing is gaining prominence.

For the first time, debt funding has surpassed the $1 billion mark in 2025, narrowing the gap with equity financing ($1.18 billion). This trend is particularly favourable for asset-heavy businesses. Notably, seven out of the top ten most-funded companies in our Venture Pulse report leveraged debt to accelerate their growth.

“Debt funding unlocks equity funding for many startups. Pure equity investors want their money focused on scaling the business and not on costs that don’t directly drive growth. By raising debt, startups can cover those needs, then pay it back while preserving ownership. This, in turn, makes them more attractive to equity investors and ultimately increases equity financing for African startups,” said Frank Samuel, Investment Associate, Sahara Impact Ventures. However, Samuel warns that reliance on debt may stifle innovation as companies prioritise near-term returns over the long-term development that innovation demands.

4. Nigeria raises the least amount of funding in the big four

The big four raised a combined $2.4 billion out of the $2.8 billion raised so far. Kenya and South Africa took the lead with $879 million and $848 million raised, respectively. Egypt raised $561 million, while Nigerian startups raised the least amount in the big four, with $186 million.

Nigeria’s early-year momentum tapered, while South Africa and Kenya have hosted most of the mega-rounds and significant buyouts so far. This is in contrast to Nigeria’s performance in the previous year. Between Jan-Aug 2024, Nigeria raised the most funding amongst the big four, raising $353 million. It placed second and third in the same period in 2022 and 2023 with $974 million and $477 million, respectively.

5. A persistent Gender gap in funding.

Despite some progress, male-led teams captured 75% of all VC funding so far in 2025; female-led and mixed-gender teams received the remaining quarter. On average, over the past five years, male-led teams have secured nearly 90% of total funding. This figure, though marginally better than the five-year average, demonstrates that systemic barriers to capital remain.

"Investing in women catalyses economic growth, improves household welfare and drives transformative social change,” said Linda Davis, Founder and CEO Giraffe Bioenergy.

6. Acquisitions are a growing exit strategy.

So far in 2025, 40 acquisitions have been recorded, putting this year on course to surpass last year’s tally of 42 deals and potentially setting a new record for the highest number of acquisitions ever seen on the continent.

This includes Meta's acquisition of Egyptian AI firm PlayAI, Lesaka's purchase of South Africa's Bank Zero and Nedbank's $93 million acquisition of payments fintech iKhokha , one of Africa's largest fintech buyouts.

Acquisitions have been dominated by the fintech sector, which accounted for nearly half of all M&A deals on the continent this year, with 15 out of the 40 acquisitions going to this industry. Other active sectors include jobtech, mobility, and professional services, but fintech remains far ahead, driven by companies’ need to rapidly expand market reach, secure regulatory advantages, and consolidate infrastructure.

In terms of geography, the big four: Egypt, South Africa, Kenya, and Nigeria have witnessed the highest concentration of acquisition activity, with Egypt and South Africa leading the charge due to their mature startup ecosystems and access to capital.

7. Six startup closures so far

Six notable startups have closed their doors so far in 2025. Even with capital rebounding, not every sector escaped the storm: from Edukoya ’s digital classrooms and Medsaf ’s pharma supply chain to Afristay’s African Airbnb, Okra ’s banking APIs and cloud services, Nigeria’s payroll disruptor Bento , and Kenya’s LipaLater , these six notable ventures shut down.

The outlook for 2026 is resoundingly optimistic among investors and founders alike. According to Frank Samuel of Sahara Impact Ventures, the combination of a greater appeal for VC investments in Africa and the recent closing of multiple Africa-focused funds has injected newfound confidence into the sector. “Yes, we expect funding to increase next year because many Africa-focused funds reached both their first and final closes this year, meaning they’ll soon begin actively deploying capital,” he said.

Samuel also believes that the continent will see an influx of impact funding in the new year. “Africa is the biggest region for impact in the world today, and so we are obviously going to see more impact funds come into the continent,” he said.

If current trends hold, the continent’s tech ecosystem will not just exceed last year’s fundraising but enter 2026 with a deeper capital base and a renewed sense of its role in global innovation.